|

stocks & Markets blog |

|

It’s not difficult to have noticed that the Video/Computer Gaming sector is utterly flying at the moment and sadly I have missed out on the run so far, but I suspect there might be more upside if the right Stocks are chosen. Before writing the recent Stock Idea Blog about Gateley GTLY, I had a quick look at some Video Gaming plays and ended up dismissing them and deciding to work on GTLY instead. Anyway, since that I have reconsidered the situation and if I can find something suitable then I might put some dosh into the chosen Great White Hope.

My thinking for this Blog is to do a very high-level look at the potential Video Gaming Stocks that I can identify and after this I might decide on a particular one and do a further more detailed Blog about that chosen Company. I am not sure when this will happen and of course it is highly possible that I decide that none of them really grab me.

I will do a short piece on each Stock I look at and from the off there are 2 Stocks that are sort of in this sector but which I do not wish to include – Games Workshop GAW and Future FUTR. Both of these are very good companies and probably have upside but I don’t really see them as quite close enough to a proper Video Gaming play – FUTR is really a Magazine Publisher and does stuff that is nothing to do with Video Games as well and GAW is a bit more about a form of Games that is in the real world as opposed to the virtual world. GAW is doing more stuff regarding online but it is not pure-play enough for what I am after.

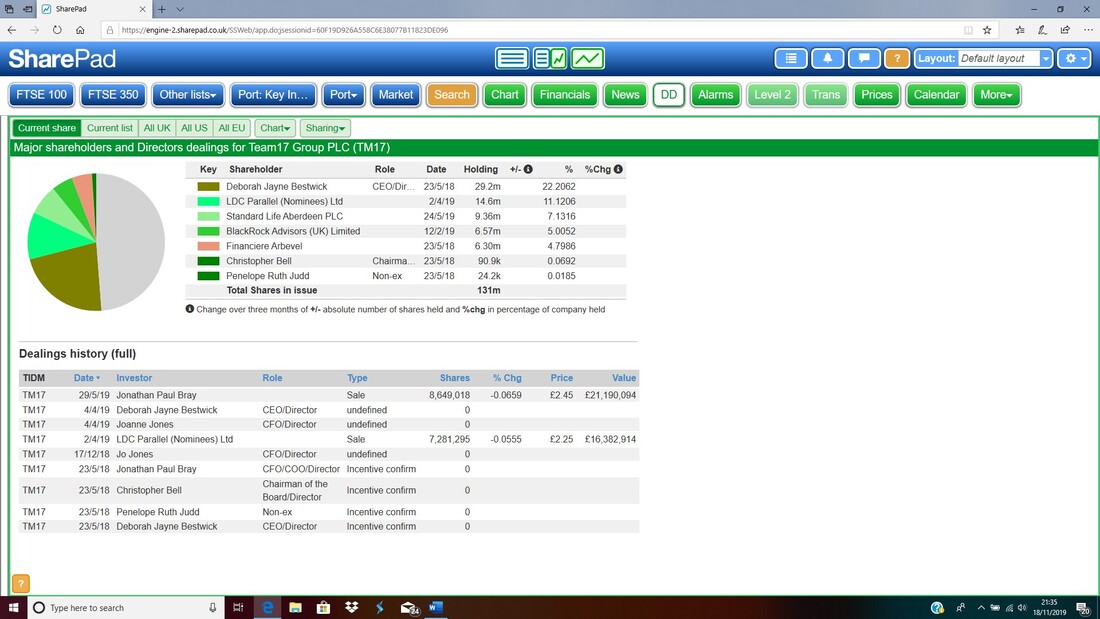

There are also some tiddlers where a Stock like Gfinity GFIN stands out and is highly unusual because it is involved in the new phenomenon of ‘E-Sports’ which is essentially Video Gaming fans all over the world watching the Superstars of the Video Gaming sphere playing their particular title of choice and the fans can pick up tips and ideas etc. to improve their own gameplay skills. I guess the moniker E-Sports is very apt because it is quite similar to a kid who loves playing football his or herself, watching the professionals play on the box. GFIN is not something I would buy yet though as it is very unproven and the track record is not great – just look at the chart and you will see what I mean. It is very rare that I will buy a Loss-making Stock and if I do they need to be close to profitability and have the revenues and growth to make that credible. OK, better get stuck in………oh, any images I show are probably taken from SharePad and if you click on them you should be able to see more details. Team 17 TM17 This one seems to be a Games Publisher and a big positive is the wide portfolio of Games that they are involved with – a big risk for Video Games businesses in the past has been that they are too dependent on just a few Titles and this can make the Earnings highly volatile. In the Trading Update from 4th November 2019 they have this text at the bottom: ‘About Team17 Founded in 1990, Team17 Group plc is a leading international premium video games label and creative partner for independent developers. The portfolio comprises over 100 games, including The Escapists, Genesis Alpha One, My Time at Portia, Overcooked, Yoku's Island Express, Yooka-Laylee, the Worms franchise and many more from developers around the world. Visit http://www.team17.com for more info.’ And rather impressively they say the following: ‘The Company has continued to experience strong customer traction from both new and established games throughout the second half of the year and now expects both adjusted EBITDA and revenue to be ahead of market expectations for the current year. The performance has been driven by continued sales momentum across the portfolio of titles.’ So that is very strong and it means that the previous Forecasts and, more crucially, the previous Valuation are off the mark and the Stock is more attractive on that basis than prior to the Update. Of course the Shares have move up since that so we need to make a judgement about the future trajectory of Earnings and ultimately the Share Price. From a previous perusal of TM17 I noticed a chunky Director Sale and on this Screen from SharePad you can see it, but also note the CEO, Debbie Bestwick, has a nice big stake:

It turns out from reading the RNS Items and a particular one from 23rd May 2019, Paul Bray and Kelvin Aston were former members of the Management Team who have since left the Company and have no involvement any more. Obviously we need to weigh this up but it looks to me like something that is not too worrying and does not put me off TM17.

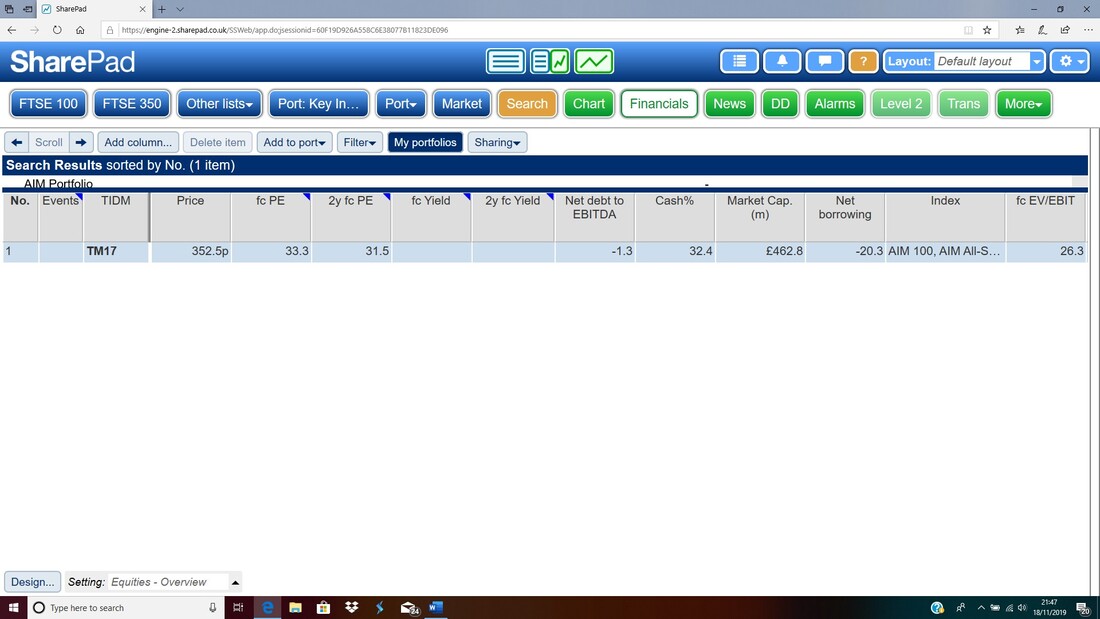

In a News item from 31st October 2019, Jo Jones the CFO had handed in her notice and it says she is going to join another Company but the information on the RNS is quite limited. Since that an Interim CFO has been found. This could be a concern and is something I would like to get more background about. The Screen below is the ‘List’ Screen from SharePad and this one can be configured as you see fit with different Columns and stuff. Anyway this shows me quickly that TM17 is on a Forward P/E of 33 dropping to 31.5 two years out – so it can hardly be called ‘cheap’ but in the current world of meaty Ratings it is not excessive. And I can also see from this Screen that TM17 had Cash at the last Results (the negative ‘Net Debt’ figure shows this). A quick look at the ‘Half Year Results’ from 10th September 2019 shows they have Net Cash of £35.8m and this is up a lot on the prior period. That’s impressive and if you strip that out then the P/E Valuation of TM17 is a lot lower.

The next image shows the Forecasts that are in the system. Compared to the quite high P/E we discussed just now, these growth rates look quite pedestrian and suggest some degree of over-valuation. However, remember they have ‘exceeded expectations’ on the latest Update so there must be a decent chance they can outperform again. Buying now is partly a play on such an outcome I would suggest. Ideally for a P/E up around 30 you would want to see 30% growth in Earnings etc.

I took the Chart image below on the evening of Monday 18th November and it might have changed by the time you are reading this. The Uptrend Channel that is marked by the Blue Shaded Zone is something I lazily used via the SharePad ‘Add’ Menu (go for ‘Trend Line’ and then ‘Confidence Line’) but it is obvious that TM17 has been in an Uptrend since it IPO’d back in May 2018. It looks like it Floated at about 195p so it has added about 85% since then so early buyers must be quite happy. It is a nice trend though.

In conclusion there is a lot to like about TM17 but that exit of the previous CFO is a concern and I need to find more information about that. There are concerns about the Valuation which need to be weighed up, although that might not be a killer for an investment but the Chart looks pretty nice and we know it is a hot sector. This one is definitely a candidate for me to investigate deeper.

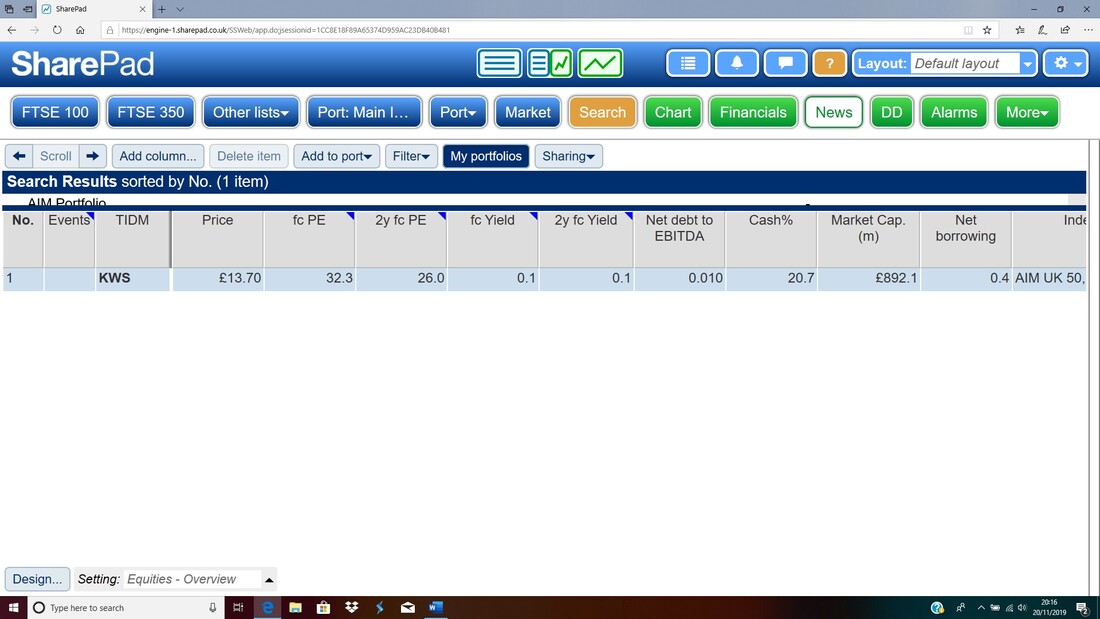

Keywords Studios KWS This one is a bit more ‘Picks ‘n Shovels’ and from what I understand it provides various Development Services to Companies that publish Video Games, which can take the form of things like Language Translation, Artwork and Design, specialist animation skills etc. etc. The twist (or sting) in the tail is that they have grown extremely fast by acquisition and so far this has gone very well. Of course this is a very risky strategy and brings potential for trouble although so far they have been very much about small ‘bolt-on’ acquisitions and in reality the more they do it, the better they probably get at it. I am cautious about this strategic approach but it is not the Red Flag for me that it is for many Investors. There is a considerable risk around being a Games Publisher and this is especially the case if you only have a small number of Games Titles. Going for a Picks n’ Shovels play could be a really good idea as it avoids this huge risk that has sunk many Games businesses in the past (although to be fair, most Games Publishers appear to be more established and have decent portfolios of Titles these days and the advent of other platforms like Apps and SaaS and considerably faster hardware, has changed the Market in many ways). KWS put out ‘Half Year Results’ on 18th September and these quotes hit me: Andrew Day, Chief Executive of Keywords Studios, commented: "The Group grew very strongly in the first half with increased demand across all of our service lines, and particularly strong performances from Functional Testing and Game Development, as the market accelerates its use of external development and service partners.” I always love to see the word “accelerate” in an Update (thankfully I have never seen this word used in relation to Net Debt but no doubt some numpty management will do it at some point !!) and that suggests a strong background market for KWS. The shares fell on this Update but when you read this it doesn’t seem too bad. Debt increased to EUR9m but that is still tiny and the investments in expanded facilities and more staff is likely to pay off: "We invested in capacity to match this accelerating trend, with significant investments in new and enlarged and improved facilities which will come on stream incrementally during the second half and into 2020. This investment, combined with a ramp up in staffing to meet faster and earlier growth than previously expected in our Functional Testing service line, meant we carried additional direct and indirect operational costs in the first half. However, underlying margins remain in line with historic norms and we, therefore, expect margins to progress in the second half and through 2020 as we benefit from our first half and ongoing investments.” "Trading in the second half has started well, with continued strong performances from our Game Development, Functional Testing and Art Creation service lines in particular. Overall, this leaves us well placed to deliver revenues for the full year at the upper end of current market expectations with our profit expectations broadly unchanged.” Slightly worryingly I spotted 2 errors in that text – one spelling and one format/grammar – which hopefully doesn’t reflect the standards of their work !! In terms of Valuation the next screen gives some pointers:

Note the Cash% is incorrect now (SharePad bases such numbers on Full Year Results I think) but a Forward P/E of 32.3 falling to 26 doesn’t strike me as too rich for something with such growth potential. I am quite taken by this Stock really. Oh, there is not much Dividend but to be fair it is probably better for the Management to focus Cash resources on growth at this stage rather than on payouts to Shareholders.

For the benefit of Readers, here is the ‘Forecasts’ screen from SharePad:

All these SharePad images were taken on the evening of Wednesday 20th November 2019. It’s quite a nice Chart as shown below. The key here is the Long-Term Uptrend Support Line which is in Red and marked by my Red Arrow and look how the Price dropped back and then bounced and formed the move up captured in my Black Ellipse. Up above we have the Green Resistance Line (marked by my Green Arrow) and this might prove troublesome in coming periods. If it can get above the Green Line that would be bullish.

Frontier Developments FDEV

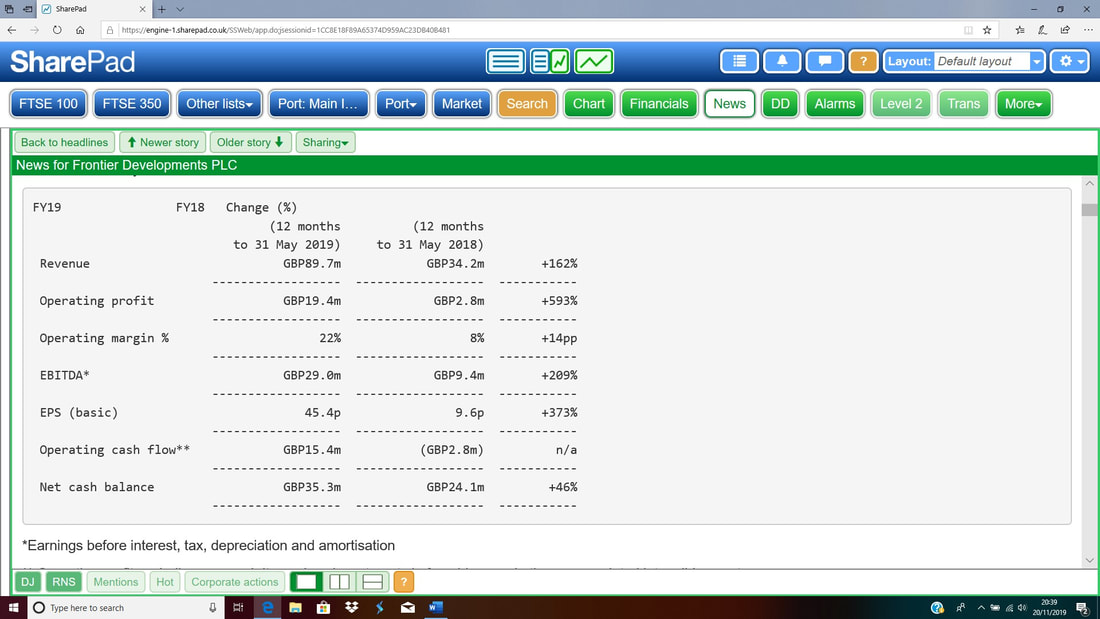

This one is a Games Developer/Publisher and has done well on the Share Price although it has dropped back from the peak – but it is clearly doing a lot right. This text from the ‘Trading Update and Product Roadmap’ from 15th November 2019 succinctly tells us what they do: “Frontier has a proven track record of launching multiple genre-leading game franchises with a strong post-launch nurturing strategy, supporting and expanding on the initial releases to deliver multi-year revenues. Frontier has launched and nurtured four successful titles to date since transitioning to self-publishing in 2013-2014; Elite Dangerous (December 2014), Planet Coaster (November 2016), Jurassic World Evolution (June 2018) and Planet Zoo (November 2019).” This chunk implies they are doing ok: “Current trading and outlook Taking into account the strong launch sales and the anticipated performance of Planet Zoo, together with the ongoing contributions from Elite Dangerous, Planet Coaster, and Jurassic World Evolution and all support and expansions, the Board continue to be comfortable with the current range of analyst revenue projections of GBP65 million to GBP73 million for the current financial year 2020 (the 12 months to 31 May 2020).” It is also clear that they have plenty of planned Game Releases lined up and this should help bring Revenues and Profits in and also plenty of News is likely to keep Investors excited about the Shares. On 4th September FDEV issued ‘Unaudited Annual Results’ and this bit of text looks hugely impressive – especially the Cash increase. Obviously there are timing issues here and it is by no means certain that such increases in Revenue etc. can be produced year in, year out. That is in the nature of these kinds of companies where Revenues and Profits can be hugely affected by the timing of new Product Releases.

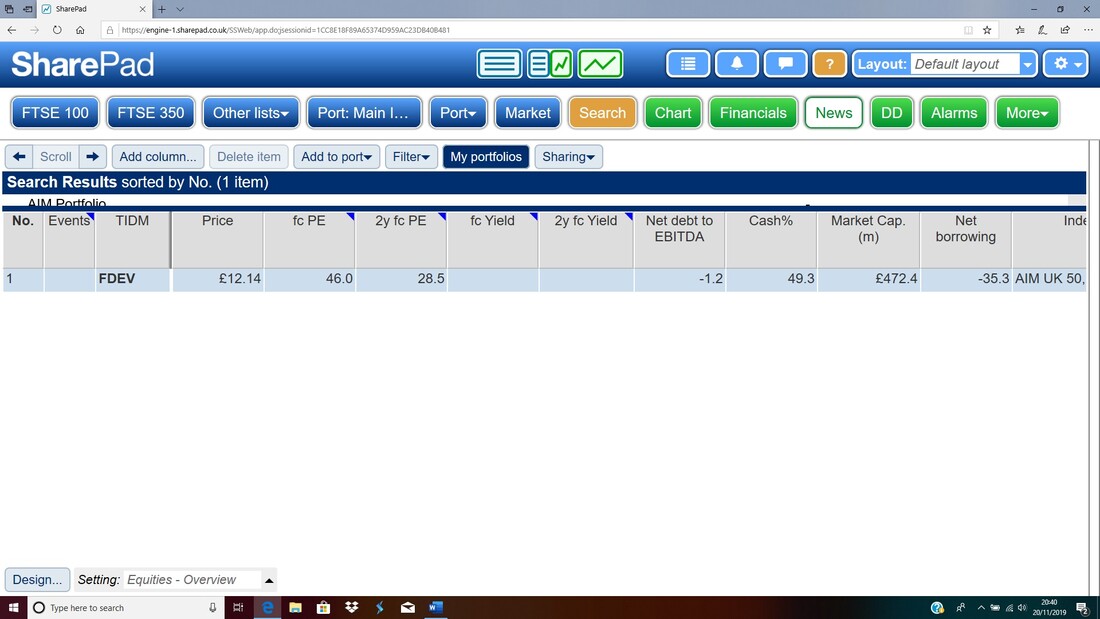

Again I have taken these SharePad images on the evening of Wednesday 20th November 2019, and my Screen below has the Valuation stuff for FDEV. A Forecast P/E of 46 is clearly very high and this is expected to drop to 28.5 in 2 years which has delivery risk around it. Remember FDEV had £35.3m Cash at the FY Results (from the table above) and this might even be higher now so if you strip that out the P/Es are a bit lower.

It is hard to claim this is a bargain though. I wouldn’t say it is overvalued but it is certainly pricey although Long-term Buyers who can accept that the ride might be choppy could do very well buying now – and of course a ‘stake-building’ strategy where you average down as appropriate could work very well on a long-term view. We know Video Gaming is a high growth sector so high Valuations are to an extent no surprise – however, other Stocks in my Blog might be a bit more appealing on the Valuation side of things.

This screen on Major Shareholders is interesting. Clearly the CEO holds loads and the presence of Tencent on the list is intriguing:

Another interesting chart. Again my Red Support Line (Red Arrow) is important and shows the Trend is upwards and this time we have a nearly parallel Green Resistance Line up above (marked by my Green Arrow) and this looks quite a nice Channel that the Price is wiggling around in. Of course it must stay above the Red Line.

The Chart is quite similar to that on KWS and after peaking where my Black Ellipse is it fell back and now seems to be steadily crawling back up again. From this quick whizz round I can see a lot of attractions in FDEV and it defo deserves consideration. The Valuation is meaty though and that might swing it for me.

That’s it for Part 1 and I have found this a useful exercise in formally looking at the options in the Video Gaming sector and doing it in this structured manner is without doubt helpful for my decision making. I have some favourites already but chances are the Stocks in Part 2 will throw up some candidates as well. In theory I will do a Conclusion and plump for one of them and I will be looking to buy something quite soon.

Cheers, WD.

0 Comments

Leave a Reply. |

Stocks & Markets WheelieBlogsThese tend to be more Markets and Stocks related and timely - the Blog Page on the Main WheelieDealer Website has the 'Educational' stuff (well that's the theory anyway !!). Archives

October 2021

Categories

All

|