|

stocks & Markets blog |

|

This Blog 2-parter is looking at a high level at the decent Listed Stocks related to the Video/Computer Gaming sector with a view to me choosing one for further in-depth Research and ultimately tracking down the best one as I see it to buy. To be fair, of the 3 I looked at in Part 1 they all look quite good although a common issue is high valuations but that is something I can live with, as long as I am buying something where the quality is high and I can see it having long-term endurance. You can find Part 1 here:

https://wheeliedealer2.weebly.com/stocks--markets-blog/video-gaming-sector-part-1-of-2-including-tm17-kws-fdev Now I will look at a couple more.

Codemasters CDM

I am typing this on the evening of Tuesday 26th November 2019 and earlier this morning CDM issued Interim Results. Before we look a bit at those, I will just highlight that CDM is a Games Developer and Publisher that concentrates on ‘Racing’ Games and its shining star is a licencing deal with Formula 1 so that it produces the Official F1 Game. This was recently extended to 2025 although it does present a Risk, albeit perhaps not particularly high due to an element of ‘lock-in’ and inertia, that at some point the relationship could end and CDM would lose a major franchise. CDM have held this Licence since 2009 so it is well established. CDM listed back in June 2018 so it has not been on the Market for long and we will look at the Chart in due course – although a simple summary would be to say that the Share Price has gone mostly sideways since that time. This simple one line from today’s results tells me a lot: ‘-- Revenues of GBP39.8 million with one game release in H1 2020 (H1 2019: GBP39.7 million with two game releases)’ From just this piece of the jigsaw it stands out that CDM is very dependent on its Release Schedule timing and this will mean that Results are likely to be ‘lumpy’. As a rule, lumpy businesses should be on lower P/E Ratios than ones where the Revenues, Profits, Cash-Flows are more stable and predictable. These Gross Margins are super-impressive – but of course it is no huge shock as with the nature of these things once they have created the Software for the Game Release, the additional costs (marginal costs) for each new Customer who takes the Release is negligible. The classic example of this is the Nail Factory – it needs a huge amount of Capital and effort to build a Nail Factory to make just one Nail but after this the Costs per Nail utterly tumble. High Margins should be a feature of any Publisher in this field: ‘-- Increased gross margin of 89.0% in H1 2020 (H1 2019: 88.5%), underpinned by continued digital sales growth, now representing 61.7% of total revenue in H1 2020 (H1 2019: 53.4%).’ Always nice to see Cash going up: ‘-- Net cash of GBP24.6 million at 30 September 2019 (30 September 2018: net cash GBP16.7 million)’ A useful back catalogue of Games should be a feature on most Gaming Companies although there is most likely a fairly short lifetime as new technology, particularly on the hardware side of things, makes older Games obsolete: ‘-- The Company's overall back catalogue (including DiRT Rally 2.0) continues to contribute significant sales, driven by growing digital demand.’ And CDM says it is ‘in line with expectations’: ‘Outlook -- The Board is confident that the results for the full year will be in line with its expectations.’ As always, the images I show are taken from the sublime SharePad software I subscribe to and if you click the pictures they should get larger so you can see the detail better. The next first image shows the SharePad ‘List’ Screen for CDM and I am actually very surprised by the Valuation implied by these Forward P/E Numbers. A Forecast P/E of 16.7 next year, falling to 14.5 the year after does not look expensive at all – although bear in mind what I said earlier about Lumpy businesses. We could also strip the Cash of £24.6m out for the P/E calculation so it certainly scores on the Valuation front. There is no Dividend but with this being a fast-growth Sector that is not hugely problematic, although I am sure many Shareholders would like at least a token payment.

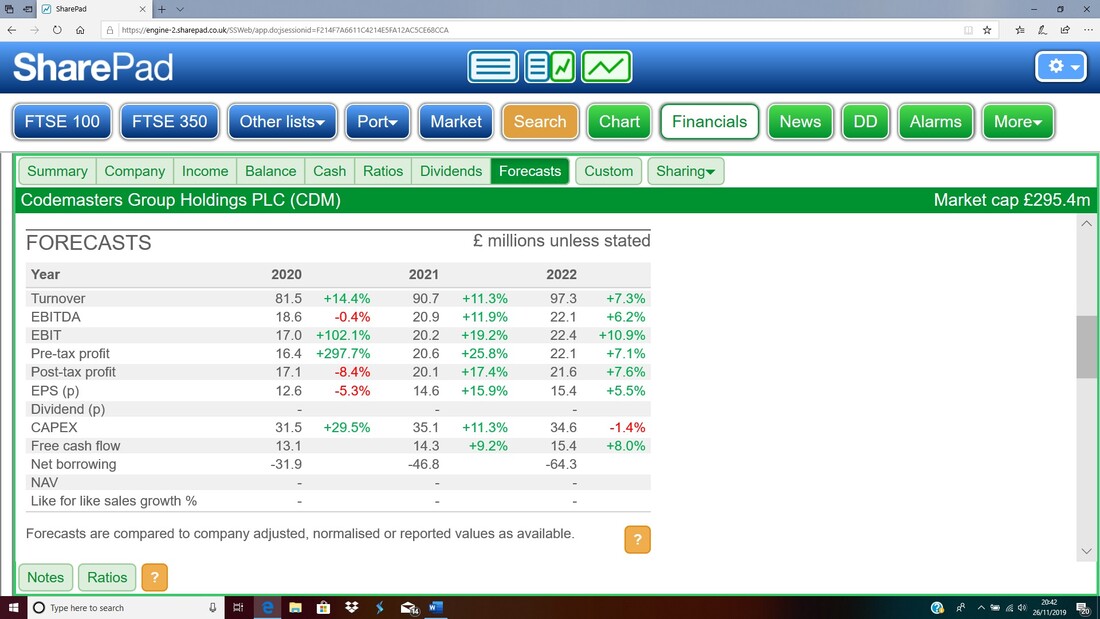

Here is the ‘FORECASTS’ Screen from SharePad as I am sure Readers will appreciate this:

This Chart goes back to the IPO date and the main things to notice here are the Black Top Resistance Line (marked by my Black Arrow) and the Red Support Line at the bottom (marked by my Red Arrow) which is ‘squeezing’ the Price in a good way for Bulls and as long as Support from this Red Line dominates, then it is highly possible that the Price will get squeezed until it ‘pops’ out of the Black Line and that would be Bullish.

My Blue Arrow is trying to point out how the Darker Blue Wavy Line which is the 50 Day Moving Average has done a ‘Death Cross’ against the Lighter Blue Wavy 200 Day MA Line. That is not so good but it is a very ‘slow’ Indicator and if the Price can perk up soon then it might avoid any weakness in coming months. The key is really that Support Level at about 190p (I deliberately pointed the Red Arrow at this) and as long as that holds there is not much for Bulls to worry about.

Sumo Group SUMO

This one is more like Keywords Studios KWS in that it does Services and stuff for the Games Publishers. Again this has not been around all that long having Listed in December 2017, but it is most definitely an interesting Chart as I will show in a tad. There was an interesting development here where Tencent took a 9.96% Stake in SUMO on 15th November 2019 and they bought it off Perwyn as follows from the RNS: ‘The shares are being acquired by Tencent from Perwyn, an evergreen, family-funded private equity business and investor in Sumo Group since September 2016. Following the sale of these shares, Perwyn will retain a 17.38% interest in the Company.’ Tencent is obviously a big player and this has to be a positive sign, and this statement from the RNS gives more of a high-level flavour of what SUMO is about and clearly it is very similar to KWS: ‘Carl Cavers, Chief Executive Officer of Sumo Group, said: "We are delighted that Tencent have chosen to acquire a shareholding in the Company, and we look forward to working with Tencent to explore co-development opportunities. When Perwyn invested in Sumo Digital in September 2016 we were a private company with annual revenue of around GBP24m and operated from three studios in two countries. We are now a public company and, following the recent announcement of our new studio in Warrington in the north west of England, now have ten studios in three countries and reported revenue of more than GBP38m for the year ended 31 December 2018. I would like to thank Perwyn, once again, for their original investment and for their ongoing support of the business." ‘ SUMO had Half Year Results on 26th September and the key takeaway is that they were ‘in line with expectations’. I like the sentiment behind the following words, in essence it says to me ‘growth’: ‘During the Period, Sumo Group continued to deliver on its stated strategic objectives: to expand; to win new clients; to develop complementary new revenue streams; and to develop its own IP - both self-funded and co-funded.’ And they have Cash that is building: ‘-- Strong cash and working capital performance post Period end: net cash of GBP8.9m at 31 August 2019 (30 June 2019: GBP4.3m)’ It looks like they also develop some Games and own the IP themselves – that’s good and if they do more of this it could make them a bit of a hybrid between the KWS model and the Games Publishers like CDM, TM17 etc.: ‘-- Two own-IP games announced: "Pass The Punch" and the acclaimed "Dear Esther" expanding to iOS’ Next up a look at the Valuation and I took this Screenshot from SharePad on the evening of 28th November 2019. A Forward P/E of 24, falling to 21 two years out is not particularly an amazing bargain, but when you factor in the Cash and the high valuations generally in this sector, I don’t think it is too silly and buyers at such a level will probably do ok over time. As something to remember for future recall, it is worth appreciating that Quality Companies can grow into high valuations over time if they continue to deliver. SUMO doesn’t pay a Dividend but that is not a huge issue when they are in such a high growth market and it makes sense for them to focus their capital resources on growth. Simply put, SUMO has a strategy including acquisitions and it is probably better for Shareholders at the moment to see the Company splashing out on nice Bolt-ons rather than giving them back Cash in the form of a Dividend.

Next up I have chucked in the ‘FORECASTS’ section and it is worth noting that the Growth Rates implied here are actually pretty good and of course it they beat these then that will be very good for holders. With an acquisitive strategy it is highly possible that they can grow faster by some nifty acquiring:

The Chart below I took on the Evening of 28th November 2019 and this shows all the Chart history for SUMO since it Listed. First up note the Horizontal Black Line (marked by my Black Arrow) at about 187p and the key thing here is that this represents the Top Line of a ‘Flat Top Triangle’ which you should be able to see when you consider that my Red Line (Red Arrow) is the hypotenuse of said Triangle.

I love these Dairyleas because what happens is the Red Line at the bottom ‘squeezes’ the Price upwards and eventually it ‘pops’ out of the top and you get a big movement upwards. However, if the Red Line fails to act as support at any point, then the Toblerone is broken and you won’t be getting your pop. In general though, these Triangles are very reliable and are nearly always good news. My Green Ellipse is trying to show where the Lighter Blue Wavy Line 50 Day Moving Average is heading down towards the Darker Blue Wavy Line 200 Day MA. If they cross then it is bad news because you get a ‘Death Cross’ and it implies weakness ahead. However, such Crosses are quite ‘slow’ and it often happens where you get a Death Cross but not long after it reverses and does a Bullish Golden Cross.

When considering these Stocks I am really thinking long-term but in the case of SUMO I am sure Readers will be interested in this next Chart. This shows the Daily Candlesticks for SUMO and my Blue Arrow is pointing out that it is very near a ‘Bear Cross’ where the Black 13 Day Exponential Moving Average crosses the Red 21 Day EMA. This usually implies weakness after the Cross but note this Price has been pretty much going sideways for 5 months so you can probably see that it has been giving Bull and Bear Crosses on these EMAs all along that timescale but without any big moves really.

The key level here is 149p and if that fails then expect more trouble.

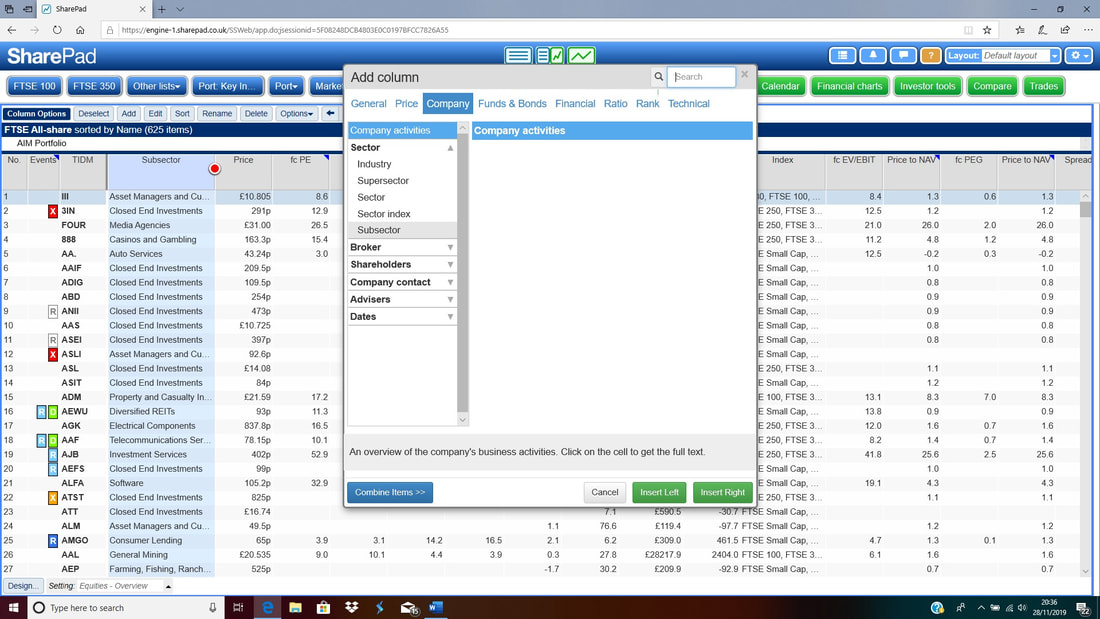

So far I have looked at 5 Companies that I knew from bumping into them before but of course I might have forgotten or missed a few more potential plays. In order to figure this out, I have gone to the SharePad ‘List’ page and clicked on the ‘Other lists’ button at the top and chosen ‘FTSE All-share’. I then realised that I did not have a Column for the Sector or Subsector or anything so I used the ‘Add Column’ button to find a suitable Description and I decided on ‘Subsector’ as you should be able to see on my Screen below:

I won’t show the full process but I then highlighted the Subsector Column and clicked on ‘Sort’ and it then instantly grouped all the Subsector Stocks together as you can probably see below. First I did this on the FTSE All-share but there were no Companies in the Video Game field there so I then chose the Aim All-share List and I got what you can see below.

From this listing, the Companies we are interested in come under the Subsector description ‘Electronic Entertainment’, which I suppose makes sense, and you can probably see from this list that I have covered all the sizeable and decent ones. Strangely SUMO sits under the ‘Software’ Subsector but the others sit here. I looked through that Subsector and there were no other Video Gaming Companies. I had often done such Searching and Sorting using ShareScope that I used to use and this is the first time I have done it with SharePad and I am pleased to report it was dead easy and the exercise I described here just took a few minutes and that included some experimentation where I was figuring out what to do. I think it is quite similar to the way ShareScope used to work for me and I have no doubt that this type of software is hugely beneficial for this kind of initial high-level analysis and saves a huge amount of time because everything is just so easy to find and right there on one tool.

Conclusion

Well that has concluded my whizz around the Video Gaming Stocks and of the 5 I have looked at I can honestly say I think pretty much any of these could turn out to be a very good investment with time and patience. They really form two groups which are the ‘Picks & Spades’ like KWS and SUMO and I quite like both of these and then we have the rest which are focused on Game development and publishing – and of these FDEV is probably the most ‘lumpy’ but the valuation seems to reflect this and CDM is very much focused on Racing Games so perhaps a bit niched and TM17 is more of an all-rounder as it has so many titles – but the valuation is stretched although the Chart is probably the best. I am sorry to disappoint Readers but I do have a favourite but I do not want to finalise my decision just yet. I am going to mull it over for a bit but I do intend to buy something out of these 5. I will produce a detailed Blog about it as well once I finally pick one out of the hat !! Cheers, WD.

0 Comments

Leave a Reply. |

Stocks & Markets WheelieBlogsThese tend to be more Markets and Stocks related and timely - the Blog Page on the Main WheelieDealer Website has the 'Educational' stuff (well that's the theory anyway !!). Archives

October 2021

Categories

All

|