|

stocks & Markets blog |

|

THIS IS NOT A TIP OR RECOMMENDATION. I AM NOT A TIPSTER. PLEASE DO YOUR OWN RESEARCH. PLEASE READ THE DISCLAIMER ON THE HOME PAGE OF MY WEBSITE. IF YOU COPY MY TRADES, YOU WILL PROBABLY LOSE MONEY. I HAVE A LARGE PORTFOLIO AND I USE DIVERSIFICATION TO SPREAD RISK ALONG WITH TRICKS LIKE HEDGING AND OCCASIONALLY BY THE USE OF STOPLOSSES - IF YOU BUY ANY STOCK YOU REALLY SHOULD FOCUS ON HOW IT FITS IN WITH THE REST OF YOUR PORTFOLIO AND KEEP RISK MANAGEMENT AT THE FOREFRONT OF EVERYTHING YOU DO. BE AWARE THAT ALL INVESTORS/TRADERS GET THINGS WRONG AND MANY STOCK SELECTIONS WILL WORK OUT BADLY.

You may have spotted that I wrote a 2-Part Blog ‘series’ about the Video Gaming Sector recently and out of the 5 pretty decent Stocks I had a quick look at, I decided that Team17 TM17 was the one I fancied the most. There are several reasons why TM17 stood out and I am sure Readers may come to their own conclusions as to which Stock is ‘best’ – but whatever Stock is chosen the tailwind in the sector is so strong that I suspect any of them will do well given time and the prerequisite patience to hold on to them. As mentioned in the Sector Blogs, the 5 Stocks split into 2 basic groupings which are the ones that actually create and publish Games and the ones that are more ‘Picks ‘n Shovels’ and provide various services to make the Games.

I like the look of both KWS and SUMO but for some reason I am more leaning towards an actual Game publisher (by the way, to some extent SUMO appears to be a hybrid of the two, or at least it looks like it might be heading in that direction). Out of these, CDM is very focused on a particular Game type – i.e. Racing Games (this is not necessarily a problem as such and I suspect it will be just fine but quite often a focus in a particular field can bring drawbacks as well as advantages), and FDEV seems a bit more ‘lumpy’ due to its Release Schedule which puts me off.

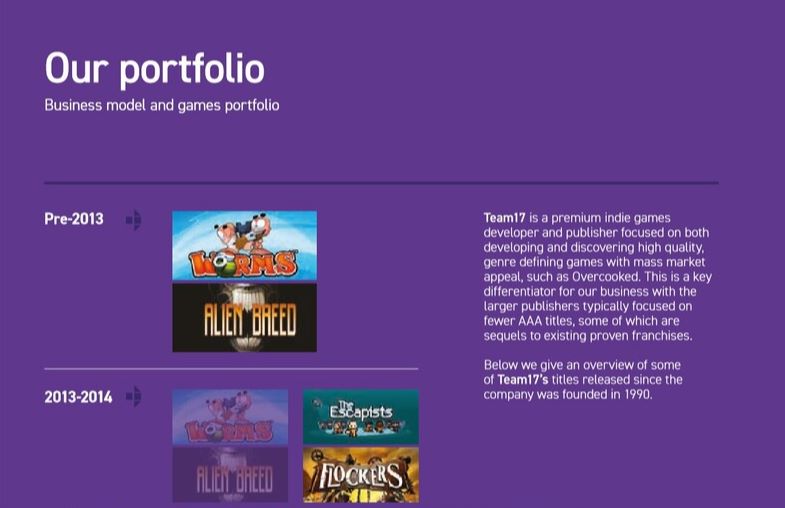

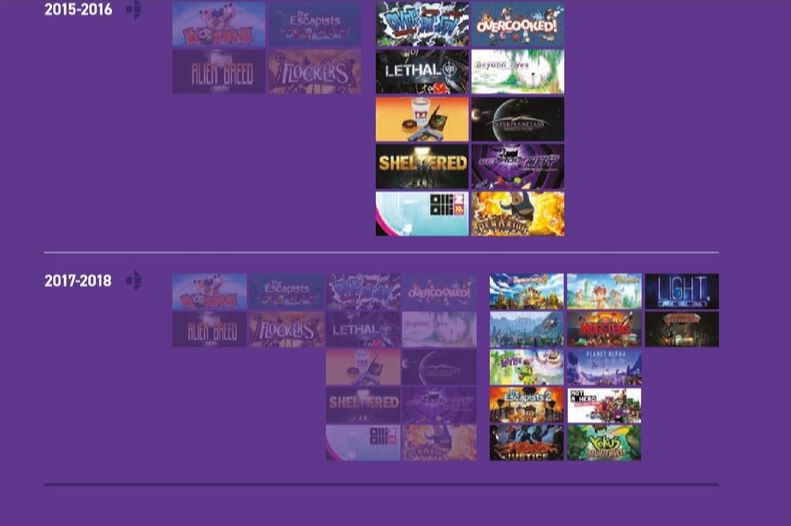

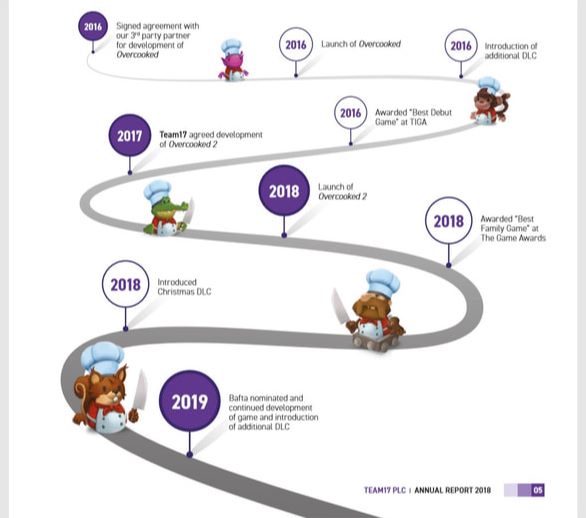

The particular attractions of TM17 in relation to the others is that it has a broader range of Game offerings so is more diversified and also the Chart looks really nice with a very well-defined Uptrend Channel since it IPO’d. I wouldn’t say TM17 is necessarily ‘cheap’ but recent Trading shows them “ahead of expectations” which implies the Stock could be cheaper than it appears and also I tend to find that strong growth plays in this sector can get away with pretty high P/E Ratings. It also has a strong Balance Sheet which is a big positive. You can find the blogs I wrote about the Video Gaming Sector here: https://wheeliedealer2.weebly.com/stocks--markets-blog/video-gaming-sector-part-2-of-2-including-sumo-cdm Company Overview The Admission Document for when TM17 listed on AIM starts off with the following text as a high-level overview: ‘Team17 is a leading video games label and creative partner for independent (“indie”) developers. The Group supports both owned first party IP and third party IP – through partnering with indie developers globally – in the development and publishing of games across multiple platforms typically for a fixed revenue share. The Group focuses on premium, rather than free to play games, and its portfolio comprises over 90 games, including the iconic and well-established Worms franchise, as well as Overcooked and The Escapists.’ The following text which I pinched from their Investor Website under the heading ‘Investor Story’ is a decent overview: ‘Team17 was founded in 1990 and launched its Games Label in 2014. Team17’s areas of expertise are: Product acquisition: identifying and partnering with highly creative indie developers, leveraging the Group’s highly selective ‘greenlight’ process to identify, screen and appraise potential titles. IP & product incubation: a 100+ employee internal creative development studio providing essential resources including additional code, art, audio, design, quality assurance, usability, release management, cross-platform development and support services. Go-to-market execution: Team17 uses the experience, skill-set and know-how within its separate commercial team to create consumer awareness and discoverability on digital distribution platforms through sales, marketing, events, public relations, social channels and community marketing. Lifecycle management: maximising long term enhanced revenue of games through dynamic price management, incremental downloadable content, promotional planning and strategic additional platform releases. 90 per cent of the Group’s revenues are generated from digital sales, which facilitates a high level of control over pricing and game lifecycle management, with minimal additional development costs post launch. Team17 has released over 100 premium games during its history, including the highly successful Worms franchise, which has continued to generate approximately £5 million in annual revenue between 2009 and 2017. Due to the Group’s diverse portfolio of owned and third party IP, coupled with its approach to lifecycle management, a substantial portion of revenue has been generated from Back Catalogue sales (revenue from titles released in previous years accounted for 52 per cent. of 2018 revenue). In addition to this a material proportion of new releases are new titles from existing franchises (follow-on titles from existing franchises with proven audiences).’ A ‘greenlight’ process is the sequence of events that need to be followed via which the TM17 management makes a decision whether or not to go ahead with a particular new game idea. In the text within the Admission Document they added the following sentence to the paragraph above about ‘Product acquisition’ and this suggests that they are fairly careful regarding which new Game Titles they go ahead with: ‘In 2017, c.1.5 per cent. of games reviewed successfully completed the greenlight process and were signed to the Games Label.’ These graphics from the Annual Report 2018 give both an idea of the Games TM17 do but also the growth in the number of Titles they have:

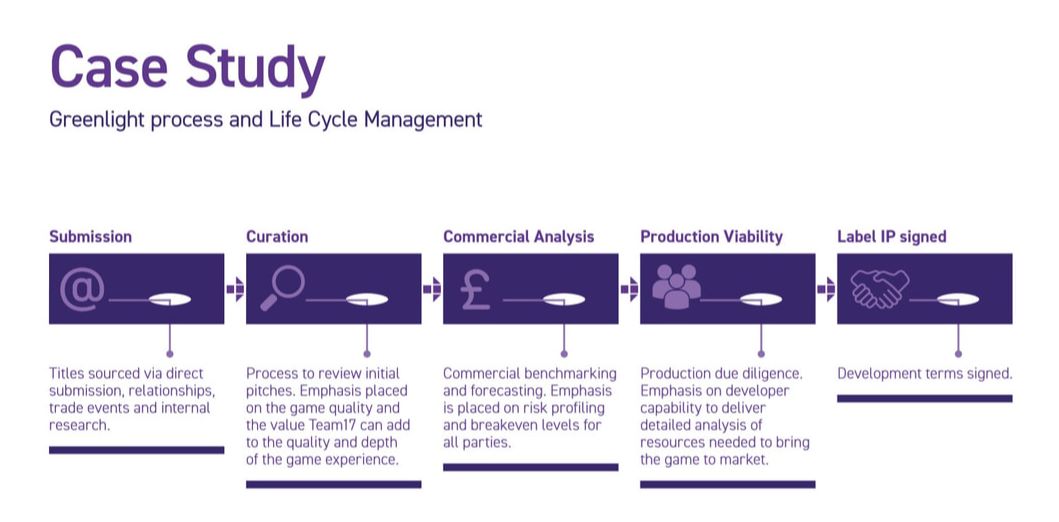

These images show the process of selecting a new Title and developing it (these are from page 5 of the Annual Report 2018):

I took the text below from page 7 of the Annual Report 2018, it suggests that TM17 use Free stuff to attract Users to the Titles and then charge for more features, higher levels etc.:

‘we continued to release new paid and free downloadable content (“PDLC”, “FDLC”) at optimum points during the lifecycle to further enhance the value and extend the life cycle of games that form part of the back catalogue.’ Company Website You can find the Investor Website here (be warned, it’s a bit heavy on the purple and very light on content !!): https://www.team17group.com/ The Consumer-facing Website is here: https://www.team17.com/ As a general ‘first look’ observation, I would say the information on the Investors bit is quite skimpy. This is not a big deal but it might be wise for the Company’s PR operation to pay more attention here !! Key Risks

Key Attractions

Company History I took the text below from the Admission Document: ‘Team17 was founded in 1990, publishing third party IP games principally for the Commodore Amiga platform. The Group released over 20 games with numerous games developers from around the world prior to the launch of Worms (including the highly successful Alien Breed franchise) and, in 1993, won the Golden Joystick award for “Software House of the Year” (jointly with Electronic Arts). In 1995, Team17 released Worms, a turn-based strategy game which would subsequently win numerous awards across all major gaming platforms. Between 1995 and 2010, the Group was principally a games developer focused on developing titles for its Worms franchise for numerous games publishers, such as Ubisoft, Sega and Hasbro. In 2011, Team17 co-founder and CEO Debbie Bestwick MBE and Paul Bray, who joined the Group in 2010 as CFO/COO, led a management buy-out which culminated in a strategic repositioning of the Group and the launch of the Games Label in 2014. In September 2016, private equity investor LDC acquired a minority shareholding in the Group. During 2017, Team17 released successful titles including The Escapists Mobile, Overcooked, The Escapists 2, Aven Colony and Yooka-Laylee, and signed nine new games developers to its global Games Label.’ Strategy/Business Model I have taken this text from page 6 of the Annual Report 2018 and it gives a good bit of detail on what TM17’s competitive advantages are: ‘Founded in 1990, we announced our Games Label in 2013 with the first game launched in 2014. Our Games Label focuses on premium, high-quality games, continually striving for innovation in gameplay and created by talented partners from around the globe. Through working with Team17, our partners have access to our award-winning development and commercial resources, helping them to compete at a much higher level than they would otherwise be able to do alone with limited budgets and resource. We focus on the global independent gaming market. The games market continues to experience strong growth due to the adoption of digital distribution and reduced barriers to entry driven by middleware gaming engines creating more accessible development tools for smaller development teams. Additionally, there is increased accessibility for customers through digital distribution platforms such as Steam, the Epic Games store, PlayStation, Xbox, Nintendo, Google and Apple stores. We have adopted a comprehensive process for identifying creative ideas and talent via our ‘greenlight process’. Games, sourced across a number of channels (including desk research, existing relationships, direct submission and crowdfunding), are comprehensively evaluated for commercial and product quality viability. Upon signing a title, we provide funding and value-added resources to our partners, with any payments contingent on achieving mutually agreed milestones to deliver the highest quality games possible within budget. The strength and depth of our skill set enables us to support our partners through all stages of game creation and franchise building. We have long established credentials in successfully building franchises and bringing high quality games to market. We have cultivated experienced teams across all areas of the business and refined the best approach across all disciplines required to deliver quality games. As such, our expertise is broad and includes:

Managing the life cycle of games ensures they continue to contribute revenues to the business as part of our back catalogue. The back catalogue, which comprises of titles released in previous financial years, is continually supplemented by new game releases. Successful games such as Worms, The Escapists and Overcooked have continued to contribute significant revenues to the business long after their initial release and have spawned successful sequels. As the games industry has evolved with the digital era, the lifecycle has also extended significantly, with a game’s success no longer pegged to boxed retail sales in the first week of launch. Franchises can be built and grown over a number of years in the digital world, and we are proud of our success in creating a number of leading franchises, and our ability to maintain strong pricing of our games in industry wide traditional discount sales windows. The access we and our partners have to these core resources enables us to continue to deliver high quality games. This is independently recognised around the world with over 140 nominations and awards across our label in 2018. We are able to deliver an end-to-end solution to our label partners and support them all the way from concept to launch, and post-launch through lifecycle management and franchise building.’ Competitive Environment / Market Unlike many Markets where there are just a small number of competitors, for TM17 I suspect the competition is utterly immense and there are countless Video Game Titles competing to grab the attention of end-users. This means that TM17 must stay innovative and dynamic and this requires highly trained and expensive employees. In that vein, I would also assume that the competition for the best developers and game designers is extremely fierce. I have taken the text below directly from page 7 of the Annual Report 2018: ‘Market dynamics The video games market continues to see significant growth and opportunities, with a recent report from gaming analytics firm, Newzoo, estimating the market will be valued in excess of $180bn by 2021. Advances in technology – both for games developers and players alike – have contributed to this overall growth, along with the ability for indie developers to realise ideas and launch games. In late 2018, Epic announced the launch of the Epic Games store, a new digital distribution platform selling to PC gamers. The Epic Games store offers significant opportunities for developers with the platform offering 88% of revenues derived from games sales. The trend of gamers accessing games via digital distribution platforms continues to gain momentum. New games launched on the leading PC digital distribution platform, Steam, numbered 7,918 in 2018, versus 560 in 2013. Due to greater access to development tools, we continue to see a large number of games submitted by developers for assessment as part of our greenlight process, but as ever our focus is on quality over quantity.’ Risks

I have taken the text below from page 10 of the Annual Report 2018: ‘Strategic Market growth and disruption – the Group operates in a dynamic industry that has seen consistent growth over many years and increasing levels of competition as the number of new games released grows year on year. This competition is multifaceted, ranging in size, sophistication and capability from large competitors to independent games developers who choose to self-publish. Slower than expected market growth or a failure to remain competitive would adversely affect the Group’s performance.

Technological change – the industry has seen some major shifts over the past few years with the shift to digital distribution along with the development of middleware such as Unity and Unreal. Ongoing technological change in both the development and distribution of games is to be expected and the Group will need to adapt quickly to these changes in order to remain competitive.

Dependence on concentrated customer base – the Group serves a small number of customers who utilise their proprietary distribution platforms to provide the Group’s games to end consumers. Any adverse changes in the status of the Group’s relationship with its customers could negatively impact financial performance.

Dependence on key titles to generate significant share of Group revenue – The Group has historically been reliant on a subset of successful titles to generate a large share of its revenues. Should the Group fail to competently manage the lifecycle of its core games this may adversely affect it financial results.

Operational The ability to recruit and retain key and skilled personnel – The achievement of the Group’s business plan is dependent on the availability of key skills and experience across its workforce. Loss of key personnel could adversely affect and impact the Group’s ability to meet its strategic ambitions.

IT security – The business is dependent on the security, integrity and operational performance of the system and products it offers. A security breach could significantly impact the business and its ability to execute on its plans.

Intellectual property – The core assets of the Group are the intellectual property it owns and that of the third-party developers on whose behalf it publishes. Any infringement to this intellectual property by unauthorised third parties may prove damaging and adversely impact the Group’s performance.

Financial / Economic Currency risk – The Group’s cost base is predominantly in Pounds Sterling (GBP) whilst its revenue is generated globally, with the largest share being received in US Dollars (USD). As such there is a risk that the Group’s financial performance could be adversely affected by unfavourable movements in foreign exchange.

Brexit – There is significant uncertainty around the impact of the UK’s decision to leave the European Union but it is likely to result in change to the UK’s economic relationships with other countries and may impact the Group’s ability to hire new staff from European Union countries which may deplete the available talent resource pool.

Why Invest in TM17? I see the main appeal of TM17 arises from the following points:

The following text comes from the Admission Document: The Directors believe that Team17 has the following key differentiators and competitive advantages: Strong market position: Team17 is focused on the premium high-quality indie gaming market, which is experiencing strong growth due to the adoption of digital distribution and reduced barriers to entry for smaller development teams through middleware gaming engines such as Unity and Unreal providing more accessible development tools. The Directors believe that the Group is strongly positioned as a games label for the indie market due to its independent heritage and its demonstrable success as a developer of award winning games. The Directors believe that Team17 has created a highly successful games label and development model, as demonstrated by its track record of successfully launching and managing numerous leading indie gaming franchises (e.g. Worms, The Escapists, Overcooked and Yooka-Laylee). Low risk approach: Team17’s business model in respect of new owned and third party IP is focused on return on investment for both Team17 and the developer. The Group evaluates potential partnership opportunities from a broad range of sources and its review process involves detailed commercial analysis from an experienced and diverse greenlight team with over 160 years of industry experience. Broad portfolio of owned and third party IP: Team17 has released over 90 games and has an extensive Back Catalogue which contributed 53 per cent. of revenue in 2017. The Group has no single franchise or title dependency and is platform agnostic, with a strong pipeline of new IP planned for launch in 2018 and beyond. Strong track record and deep relationships with key platforms: Team17 has over 25 years of experience in the gaming industry, launching games successfully onto key platforms, including Android, Apple iOS, Switch, PC, PlayStation and Xbox. Team17 has a strong track record of partnering with leading indie developers and releasing high-quality games across these multiple platforms. Experienced management team: led by CEO Debbie Bestwick, who was awarded an MBE in 2016 for services to the video games industry, Team17 has a proven senior management team with over 140 years of experience in the gaming industry, including prior experience at EA, 2K Games and Ubisoft. Team17’s internal creative studio has won numerous awards for its own created IP and has a broad range of skills, relating to cross-platform development and other added value resources such as code, art, audio, design, QA and usability. Proven financial record: Team17 has achieved strong growth in revenue and profits since launching its Games Label. Over the three-year financial period ending 31 December 2017, the Group delivered revenue and Adjusted EBITDA CAGRs of 69 per cent. and 80 per cent. respectively, with an average operating cash flow to EBITDA generation of 103 per cent. over the same period. Average operating cash flow to EBITDA generation is defined as the average over the three-year financial period ended 31 December 2017 of net operating cash flows as a percentage of EBITDA. Listing Details Index AIM Country of Incorporation England. Company Registration Number 02621976 Registered Office 3 Red Hall Avenue, Paragon Business Park, Wakefield, WF1 2UL, West Yorkshire. Subsidiary Offices From what I can ascertain, they only have the one Office location which is the one at Wakefield just above. Company Secretary I have had a good hunt around but cannot find who is the Company Secretary. There is mention of a Company Secretary having to do certain roles/tasks in the Annual Report for 2018 but no names are given. Under the ‘Contact’ section of the Investors Website, they say contact Vigo Communications, the PR Company. Nominated Advisor (NOMAD) GCA Altium Limited. 3rd Floor, 1 Southampton Street, London WC2R 0LR Broker Berenberg 60 Threadneedle Street, London EC2R 8HP Financial PR Advisors Vigo Communications Sackville House, 40 Piccadilly, London W1J 0DR Legal Advisors Squire Patton Boggs (great name !!) 6 Wellington Place, Leeds LS1 4AP Auditors PWC – PricewaterhouseCoopers Central Square, 29 Wellington Street, Leeds LS1 4DL Registrars Link Asset Services The Registry, 34 Beckenham Road, Beckenham, Kent BR3 4TU Bankers I was unable to find an answer to this item. Annual Reports As TM17 has only been listed a short time, there is not much here in terms of previous Annual Reports but you can access the one for Year Ending 2018 here: https://www.team17group.com/rns-news/reports/ If you look at the Team17 Admission Document there is a bit more Financial Information from a few previous Years. You can find that here: https://www.team17group.com/wp-content/uploads/2018/05/Team17-Admission-Document-2018-1.pdf Directors You can find the Directors with pics and profiles here: https://www.team17group.com/about-us/board-of-directors/ Quite an impressive Board really and I would highlight Non-Exec Martin Hellawell from Softcat SCT who is clearly quite switched on. He was at Computacenter CCT previously and is also involved in that Raspberry Pi thing. Jennifer Lawrence is on the Board as well but she is probably not the one you are thinking of…… The key players are as follows:

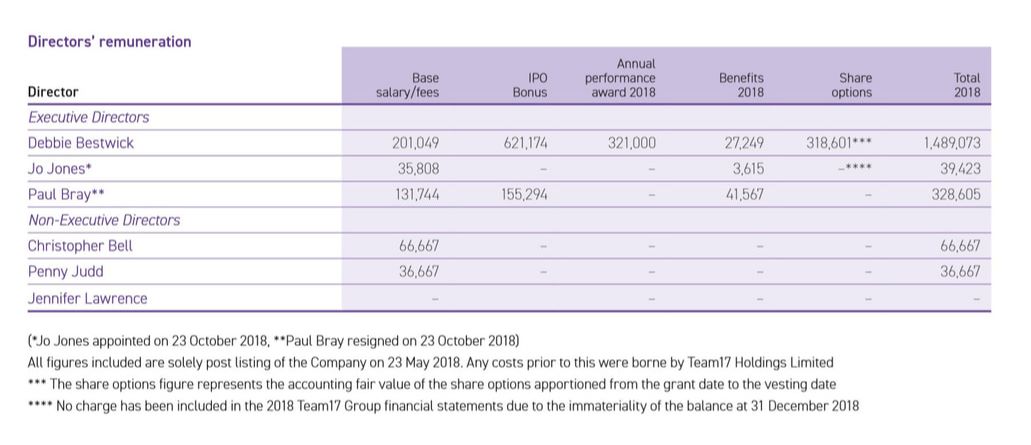

Paul Bray stepped down as Chief Financial Officer and Chief Operating Officer on 23 October 2018 and the explanation in the RNS is that he is retiring and “spending time with the family” (as they do). He joined TM17 in 2010 and saw the Company through the AIM Listing but although I find it a slight concern that they seem to get through a lot of CFOs, this doesn’t look acrimonious. You can read the RNS here: https://polaris.brighterir.com/public/team17/news/rns/story/x263glr It also talks about the appointment of Jo Jones who subsequently left TM17 on 31st October 2019 “to take up another challenge”. This RNS is a lot more brief !! https://polaris.brighterir.com/public/team17/news/rns/story/w6nkm9r Director’s Pay The following Table giving the breakdown of what Directors take home is from page 16 of the Annual Report 2019:

I don’t know much about what kind of level Directors should be paid at but from my limited understanding this doesn’t look too crazy although Debbie Bestwick does seem to do pretty well.

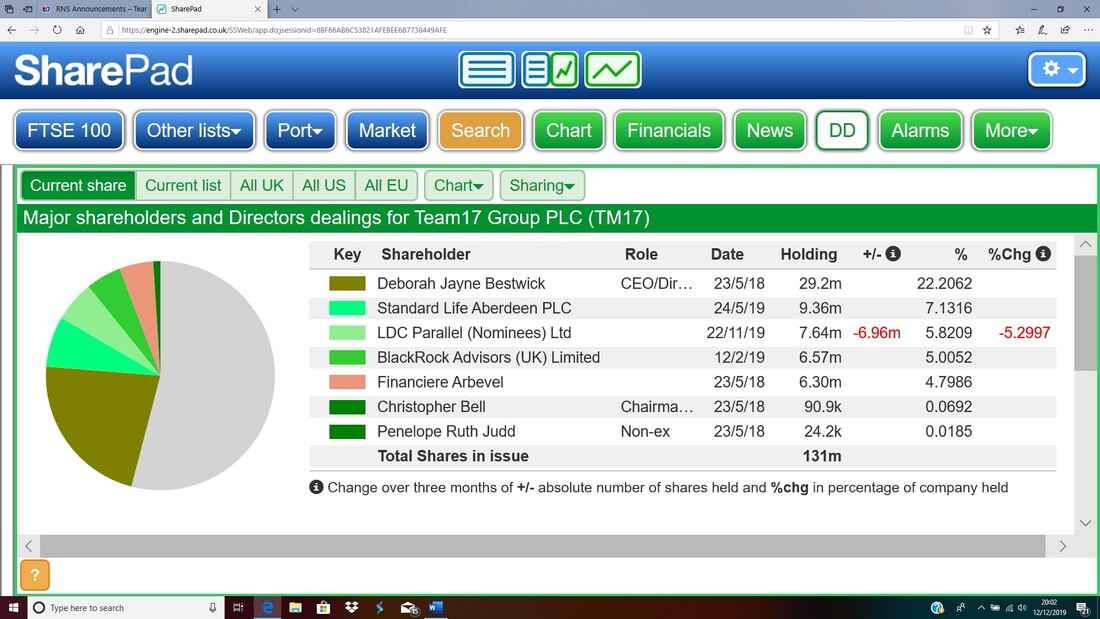

Director Shareholdings and Major Shareholders The Screen below I have taken from SharePad. I have used the ‘Ctrl / +’ keyboard function to make this image larger so it should be a nice size to see the detail:

Clearly the CEO Debbie Bestwick has a large holding and you can see where LDC have been selling down their holding as I discuss a bit further down.

On TM17’s Website you can find a list of Major (over 3%) Shareholders on this page: https://www.team17group.com/aim-rule-26/shareholder-information/ On 21st November LDC (Lloyds Development Capital) sold about one third of their Holding via an Accelerated Bookbuild. After this they hold 6.5% of the Company and there is only a 90 Day Lock-in period so more Sales are possible (I note on the ‘Shareholder Information’ page it says they hold 5.8% but this is most likely an admin error). You can read the RNS here: https://polaris.brighterir.com/public/team17/news/rns/story/w616pqx The Shares were got away at 320p as per the RNS that came out the next day and they actually shifted a few more than mentioned in the first RNS: https://polaris.brighterir.com/public/team17/news/rns/story/r7n65gw Obviously such Sales are not a hugely positive sign although of course LDC can have their own portfolio reasons for selling etc. and it is good to see that the Shares got away at a fairly good price for existing Shareholders. I saw that LDC came into TM17 after the Management Buyout and it is very likely that LDC has a Business Model whereby they invest in early stage businesses or special situations and it is their normal way of working to seek an exit once the Stock is up and listed on a Public Market. Shares in Issue I took the following text from the Company Website under the ‘AIM 26 Rule’ tab on Saturday 30th November 2019: ‘The Company’s issued share capital consists of 131,288,276 ordinary shares with a nominal value of 1 pence each (“Ordinary Shares”), each share having equal voting rights. The Company does not hold any Ordinary Shares in treasury and therefore the number of Ordinary Shares with voting rights is 131,288,276. In accordance with AIM Rule 26 in so far as the Company is aware, the percentage of the Company’s issued share capital that is not in public hands is 49.6%.’ Recent Director Dealings The Screen below is actually they bottom half of the Screen I just showed for Director and Major Holdings from SharePad. There has not been much activity and the LDC Sale I discussed above and Paul Bray left TM17 in October 2018:

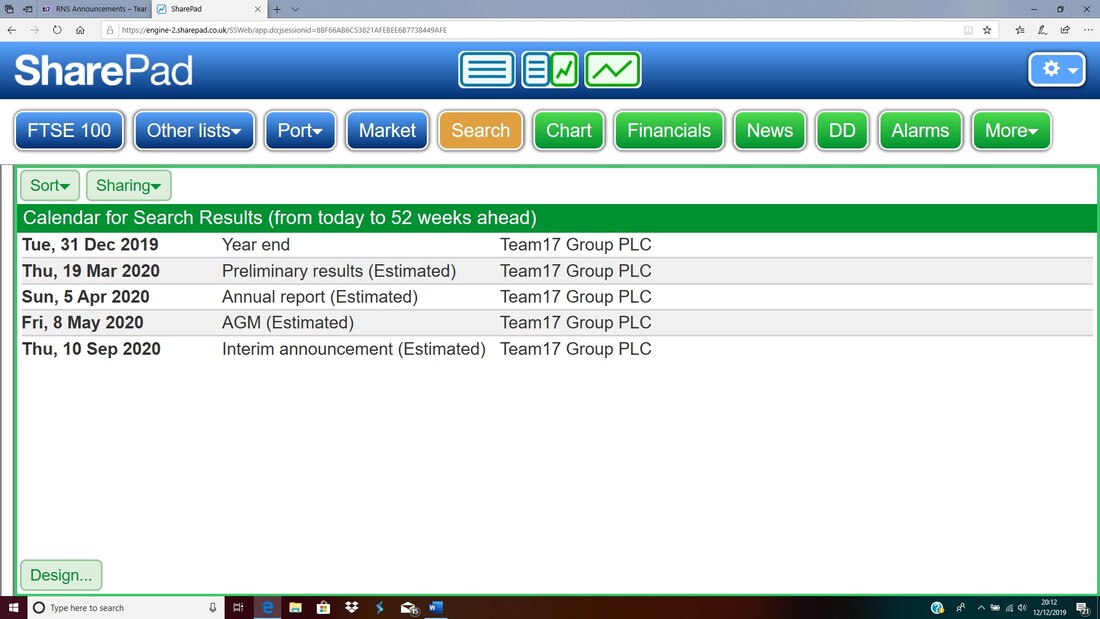

Calendar

Another SharePad screen for your delight:

OK, that’s it for Part 1. At the time of scribbling this I do not hold Shares in TM17 but that situation might change quite soon. I intend to create Part 2 over the coming week and it should get published at the end of next week.

Regards, WD.

2 Comments

Geoffers45

12/14/2019 03:30:40 am

Thanks Wheelie for such a detailed analysis.

WheelieDealer

12/16/2019 01:33:04 pm

Hi Geoffers45, thanks for the feedback, much appreciated and I hope it helps, WD :-) Leave a Reply. |

Stocks & Markets WheelieBlogsThese tend to be more Markets and Stocks related and timely - the Blog Page on the Main WheelieDealer Website has the 'Educational' stuff (well that's the theory anyway !!). Archives

October 2021

Categories

All

|